![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

REVESCO. Revista de Estudios Cooperativos. ARTÍCULOS

e-ISSN: 1985-8031

Ali Faiz

University

of Baltistan (Pakistan). Universitat

Autònoma de Barcelona (España) ![]()

![]()

Institución

Milá y Fontanals de Investigación en Humanidades. Consejo Superior de

Investigaciones Científicas (España) ![]()

![]()

Miguel Prado-Román

Universidad

Rey Juan Carlos (España) ![]()

![]()

Jose Torres-Pruñonosa

Universidad

Internacional de La Rioja (España) ![]()

![]()

https://dx.doi.org/10.5209/REVE.102799 Recibido: 09/03/2025 • Aceptado: 09/05/2025 • Publicado: 30/06/2025

ES Resumen. Nuestro objetivo es analizar la estructura intelectual de la contabilidad social, es decir, las referencias citadas en los artículos que abordan este campo, agrupándolas en clústeres y destacando aquellos estudios que pueden considerarse puntos de inflexión (la columna vertebral de la contabilidad social, aquellos que permitieron la difusión de este campo del conocimiento) o artículos emergentes (aquellos que reciben un alto número de citas en un corto período de tiempo). Se llevó a cabo un análisis bibliométrico de co-citas, utilizando CiteSpace para examinar la estructura intelectual de la disciplina, basada en 24.176 referencias citadas contenidas en 408 artículos publicados en revistas indexadas en el Social Science Citation Index y en el Emerging Sources Citation Index. El estudio identifica doce clústeres que conforman la estructura intelectual de la contabilidad social. Los resultados ofrecen una visión global del campo en términos de redes y sus conexiones, identifican las áreas de investigación más influyentes y describen la composición de las subdisciplinas que han evolucionado dentro de este ámbito. Asimismo, se identifican los artículos que pueden considerarse puntos de inflexión en la disciplina, así como aquellos que han recibido un número significativo de citas en un período determinado. Además, se incluye una agenda de investigación con el fin de orientar a los académicos en el análisis continuo de este campo en expansión, que está siendo implementado por muchas empresas para la monetización de la creación de valor social. La investigación futura debería centrarse, principalmente, en la estandarización de los procesos de identificación y contabilización del valor social, particularmente en unidades monetarias.

Palabras clave. Contabilidad social, valor social, estructura intelectual, bibliometría, tendencias, co-citación.

Claves Econlit. M41, A13, E16.

ENG Tracking the evolution of Social Accounting: intellectual milestones, key debates and research challenges ahead

ENG Abstract. We aim to analyze the intellectual structure, in other words, the cited references included in the citing papers that deal with social accounting, clustering them and highlighting those papers that can be considered to be either turning points (the backbone of social accounting, those that allowed the dissemination of this field of knowledge) or burst papers (those that receive a high number of citations in a short period of time). A co-citation bibliometric analysis was conducted, using CiteSpace to study the intellectual structure–24,176 cited references–contained in the 408 papers published in journals indexed in the Social Science Citation Index and in the Emerging Sources Citation Index. The study identifies twelve clusters that comprise the intellectual structure of social accounting. The results provide an overall perspective on social accounting in terms of networks and their connections, identify the most influential research areas and describe the composition of the sub-disciplines that evolved. Furthermore, papers that can be regarded as turning points are identified, as well as those that received a significant number of citations over a particular time. A research agenda is also included to help scholars to keep on analysing this increasing field of knowledge, which is being implemented in many companies when monetising social value creation. The research should be mainly focused on the standardisation of processes for identifying and accounting for social value, particularly in monetary units.

Keywords. Social accounting, social value, intellectual structure, bibliometric, trends, co-citation.

Summary. 1. Introduction. 2. Methodology. 3. Results. 4. Research agenda. 5. Conclusion. 6. References.

How to cite: Faiz, A.; Plaza-Navas, M.A.; Prado-Román, M. & Torres-Pruñonosa, J. (2025). Tracking the evolution of Social Accounting: intellectual milestones, key debates and research challenges ahead. REVESCO. Revista de Estudios Cooperativos, 150(1), 1-17, e102799. https://dx.doi.org/10.5209/REVE.102799.

In recent decades, there has been an ongoing debate on social and environmental sustainability (thereinafter, SEA) (United Nations, 2019). Companies are more devoted to social responsibility and incorporate the effects of their actions on these issues in their operational management and long-term strategy. This suggests that both academics and society are interested in establishing a business model that, in addition to generating profit, generates social value for stakeholders (Freeman, 1984) and emphasises the significance of measuring this value. According to Retolaza et al. (2016), social value is the economic value distributed to all stakeholders, along with the not-directly-economic effects of an organisation’s actions on them.

There are calls within the Social Accounting (thereinafter, SA) literature to undertake fieldwork studies in values-based organisations; accordingly, this paper works with social enterprises to develop SA and accountability at community level. SA is a broader framework of multidimensional approach, an extension of traditional accounting that incorporates the assessment and recording of a company's engagement with society, focusing on its socially responsible activities (Escamilla-Solano et al., 2025; Carnegie et al., 2024). According to Gray (1992), SA can create a forum for public discussion and action through the transparency and accountability process at the community level. Accountability should not be reduced to just a process of final reporting, whereby it is meaningless and empty (Zeng and Van Staden, 2024). The dialogue is developed through the SA process, rather than through the final documentation produced. Organisations can use SA to show the achievement of their objectives, create social impacts, pursue their missions and become more self-sustainable (Baker et al., 2023)

SA can have a wide range of objectives. The main one is that companies should be more focused on social responsibility, disclosure of relevant information in reporting and accountability and auditing (Gray et al., 2014). Merigó and Yang (2017) identified research dealing with SA in its various aspects. Rodrigues and Mendes (2018) studied how to map the literature on social responsibility. Kulevicz et al. (2020) explored how sustainability reports deal with socio-environmental and business issues. Sikacz (2017) organised the literature on Corporate Social Responsibility reporting. In this regard, companies should not ignore the essence of SA in comparison with traditional accounting. Organisations should jump out for the development of SA by setting higher objectives to achieve social economy goals.

The topics covered in this scientific work include stakeholder policy —the principles and strategies guiding how organisations engage with and address stakeholder interests—and practice (Dillard and Roslender, 2011; Parker, 2005), social auditing (Cooper et al., 2005; Thomson et al., 2015), micro-economy (Chaudhuri et al., 2024; Hartono and Resosudarmo, 2008; Miller and Blair, 2009), social economy (Porter and Kramer, 2011; Aguado Muñoz et al., 2021) and social value (Retolaza et al., 2015, 2020; Retolaza and San-Jose, 2011, 2018; Freeman et al., 2020; Toukabri and Toukabri, 2023; Echanove-Franco et al., 2023). Stakeholder policy and practice focuses on the implementation and regulation of accounting across different categories of organisational stakeholders, sustainable reporting and management control in accounting. This kind of accounting also covers the concept of social auditing, namely the objective to identify social needs and social equality. By means of a Social Accounting Matrix (thereinafter, SAM), researchers address the economic factor and its impact on the household economy. Finally, and most importantly, social economy and social value; a SA model creates an opportunity to move towards social entrepreneurship where all the stakeholders visualise their perceived value (Kamaludin et al., 2024; Hietschold et al., 2023)

The number of companies adopting SA has been steadily increasing in recent years. This growing adoption underscores the need to evaluate both the impact generated by these organisations and the effectiveness of SA itself (Retolaza et al., 2015, 2020; Retolaza & San-Jose, 2016, 2018, 2021). In this context, identifying the key drivers of change becomes essential to ensure the successful implementation and continued development of SA practices.

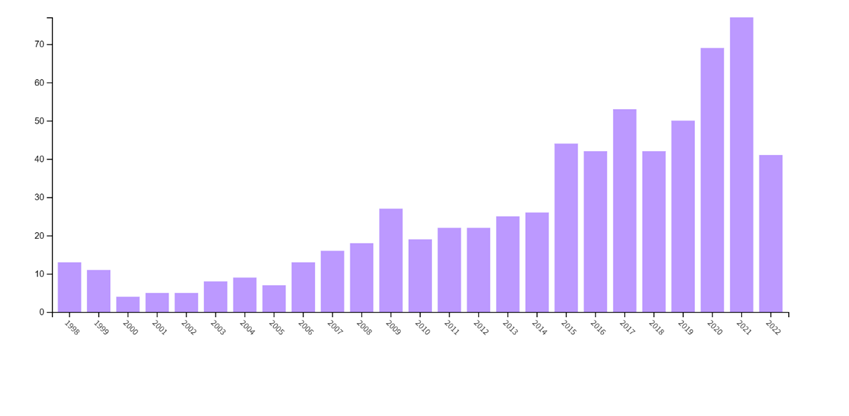

This study focuses on the period between 2013 and 2022, during which academic interest in SA has grown substantially. While data from the Social Sciences Citation Index (SSCI) and the Emerging Sources Citation Index (ESCI) indicate an annual average of only 13.3 publications between 2000 and 2012, that figure more than tripled in the subsequent decade. It is challenging to follow this expanding field of research because of the increasing number of publications on SA.

The bibliometric analysis made it possible to handle the large pool of data from hundreds of scientific papers. It provides the opportunity to assess quantitative data and deduce qualitative features. However, bibliometric techniques like the analysis of citations or co-citations require a thorough understanding of this specific area of interest. Deep understanding of the subject matter studied can be obtained through this analysis, including clustering, the identification of intellectual turning points and burst paper (the most active areas of research) detection.

The primary objective of this study is to analyse the intellectual structure, which is a bibliometric jargon word that refers to the cited references included in the citing papers of a field of knowledge of SA. While traditional literature reviews only go further into the conceptual understanding, this research contributes to the analysis of the main aspects that SA can offer as a fundamental tool to become a link between the company and society. Moreover, it presents information that will allow us to evaluate its level of commitment to the social fabric that surrounds it. This study also gives researchers a foundation for the future development of SA.

By means of the research study of the data obtained from the Web of Science a gap in the literature has been identified: the lack of a co-citation analysis on SA. Consequently, this article makes four contributions to the field, being the first paper that (1) carries out a co-citation bibliometric analysis of the academic literature that deals with SA; (2) identifies which papers can be considered the backbone of SA, those that allowed the dissemination of this field of knowledge; (3) detects which papers have become burst in the SA field, since this is a very specific feature of co-citation analysis; and (4), provides a research agenda to guide scholars in regard to future lines of research.

This paper is organised as follows: the methodology will be explained in section 2. Section 3 will discuss the results, including the clustering, the identification of the intellectual turning points and the burst areas. Finally, Section 4 suggests a Research Agenda, while Section 5 presents the conclusions and outlines a research agenda.

Scientific progress is the culmination of previous studies, the findings of which have generally been made public through countless scientific publications. No matter how specialised an area may be, there are so many publications that it is impossible to read thoroughly and evaluate methodically all of them. Therefore, it is necessary to use bibliometric techniques that perform quantitative analyses.

The bibliography shows the relationship between the author of a paper and the authors who are cited in it. Hence, the bibliometric analysis of these citations develops into a helpful tool that complements the conventional literature reviews and allows to analyse the intellectual framework or cognitive foundation that has enabled the development of the paper’s field; making possible to discover its birth and evolution, the old and new lines of research that captured the greatest interest of researchers, even the potential gaps that would be of interest to fill.

The co-citation analysis is one most reliable bibliometric methodologies to obtain a comprehensive picture of a field of knowledge (Zupic and Cater, 2015; Hota et al., 2020). It implies tracking how frequently two works are referenced together in the bibliography of a given collection of citing works (Small, 1973). Clusters of works with a common theme are built when the same pairs of works are co-cited by several authors. This reveals the interrelationships that led to the development of a scientific field, identifying lines of thought, determining the underlying intellectual framework and showing them on a visual bibliometric map. Nonetheless, it is worth noting that this technique tends to highlight consolidated contributions, as it relies on citations that accumulate progressively over time and may therefore overlook recent publications that have not yet had sufficient opportunity to be widely cited (Zupic and Cater, 2015; Donthu et al., 2021).

Bibliometric maps are frequently used as a supplement to the bibliometric analysis of co-citations. The groupings and connections in the intellectual framework of a scientific area are visually represented by these maps (Chen and Song, 2019). CiteSpace software (Chen, 2017; Chen et al., 2010) was used in this study for co-citation analysis and bibliometric mapping. CiteSpace was used in various research that look at the intellectual structure of social sciences (Díez-Martín et al., 2020; Torres-Pruñonosa et al., 2021). It is important to draw attention to the potential to identify authors and works that received a lot of attention in a certain era and, therefore, have been, are, or may turn out to be crucial for the development of SA field of knowledge (burst detection and turning points).

According to a search of the WoS and SCOPUS databases, the use of bibliometric approaches in SA was not extensively yet put into practice. Only one paper was found (Rodrigues et al., 2021) that focused on the dissemination of SA information. Although it implies the use of co-citation bibliometric analysis through Bibliometrix software based on R statistics package, our paper is the first one to use a more in-depth co-citation bibliometric analysis to identify the intellectual framework that was shaped in SA.

2.1. Data

To gather as many data as possible on a subject like SA, we choose to use in SSCI and ESCI, the following Boolean search of words in the title, abstract, or keywords (TS): “social accounting”.

On September 27, 2022, a search of the sample was conducted for the years 2013–2022, a period during which the field experienced steady and sustained growth; the results showed 408 papers with 24,176 unique references. These 24,176 references covered the whole data sample for the analysis and are related to the intellectual underpinnings of SA research. Given that the analysis is focused on the co-cited references of the 408 citing articles, where books, chapters and conference proceedings, among others, are also available, this intellectual basis extends beyond journal articles to other significant texts. This method ensures a reasonably wide source of phrases that are closely related to the area of study that will be analysed. We also reviewed the existence of different variants of a same node and used the possibility of merging, which is possible in CiteSpace, so as to obtain a more accurate network. The parameters added to CiteSpace are displayed in Table 1. To create a sufficiently coherent network where clusters are distinct from one another, even when they include comparable documents, it is crucial to give careful consideration to the node selection criteria. The g-index (Egghe, 2006) is the criterion used to choose the nodes so as to create a network that is as cohesive as feasible and in which the clusters are sufficiently distinct from one another, being also homogeneous enough and having related works (Chen and Song, 2019). CiteSpace also includes a regulation factor (k) of the overall size of the obtained network in the g-index calculation. For the purposes of this study, a k=50 has been chosen in order to produce the best suitable network.

Table 1. Parameters for the analysis

|

Parameter |

Description |

Choice |

|

(1) Timeslice |

Timespan of the analysis |

From 2013 to 2022 (27/9/2022) |

|

(2) Term source |

Textual fields processed |

title/abstract/author keywords/keywords plus (all) |

|

(3) Node type |

The type of network selected for the analysis |

Cited reference (the networks are made up of co-cited references) |

|

(4) Pruning |

It is the process to remove excessive links systematically |

None |

|

(5) Selection criteria |

The way to sample records to form the final networks |

g-index (k=50). The g index is the largest number that equals the average number of citations of the most highly cited g publications. It solves some of the weaknesses of the h-index. k is a scaling factor introduced in Citespace to control the overall size and clarity of the resultant network |

Source: authors’ own elaboration.

A recently published study by Escamilla-Solano et al. (2025) also applies a co-citation bibliometric methodology to explore the intellectual structure of social accounting research using the same keyword search in the Web of Science Core Collection. However, there are notable methodological differences that may influence the scope and nature of the findings. While their study filters results by the "Business Economics" category, our analysis includes records indexed in the SSCI and ESCI without filtering by subject area. This broader inclusion reflects the multidisciplinary character of SA, which is frequently discussed in journals beyond business and economics. At the same time, we chose to limit our dataset to SSCI and ESCI to maintain quality and avoid the inclusion of grey literature that may appear in other Web of Science Core Collection sections. Another key difference lies in the time coverage: Escamilla-Solano et al. (2025) conclude their dataset in 2021, whereas our study includes articles up to 2022, capturing more recent developments. Additionally, while they apply a scaling factor of k = 15 in their g-index configuration, we used k = 50 to generate a broader and more detailed network. Importantly, this higher value did not compromise the quality of the network; on the contrary, the structure obtained exhibited high modularity and strong internal cohesion across clusters. Despite the validity of both approaches, the results differ. Escamilla-Solano et al. (2025) identify four clusters and eight burst papers, whereas our study identifies twelve clusters and 16 burst papers. Moreover, our analysis also highlights intellectual turning points—an aspect not covered in their work—which offers additional insight into the evolution of the field.

In 2013 and 2014, growth in social accounting publications was moderate, with annual outputs rising from 24 to 26 papers (Figure 1). However, between 2015 and 2018, the field experienced a significant expansion, averaging 43.75 publications per year. This upward trend continued from 2019 to 2022, culminating in 67 papers in 2021 and reaching 76 in 2022. This research was mainly published in “auditing and accountability”, “economics”, “energy”, “business review”, “psychology”, “management and policy” and “tourism management” journals, according to the Web of Science categories. The 446 papers that were published between 2013 and 2022 represent 44.6 publications per year. Evidence that a field of knowledge was developing in SA can be found in the publication of articles in journals listed in the SSCI database, or in other words, in high-impact journals. But to what extent? This paper's third section's goal is to answer this.

Fig. 1. Growth of publications on social accounting (1998–2022). Chart shows data as of the end of February 2023. At the time of data retrieval (9/27/2022) the data for 2022 were slightly lower. Source: authors’ own elaboration.

3.1. Main Research Areas in Social Accounting

Table 2 summarises the broadest areas of knowledge and study for SA. The network is distributed into 12 significant clusters numbered between 0 and 11. Each co-citation cluster is associated with a specific structure or theme. The clustering data reveal the effects of future research studies. For example, cluster #1 in this study consists of 60 research articles. This indicates that many later academicians and researchers used these 60 publications as a single source of knowledge and information. Therefore, such clusters are considered as a framework of associated structure themes. Even if previous authors may have believed that their research contributed to a particular topic framework, their work ends up being used in specific ways, sparking new avenues and clusters.

Table 2. Main research areas in social accounting

|

Cluster |

Size |

Silhouette |

Mean(year) |

Label |

Description |

|

0 |

60 |

0.893 |

1994 |

Social Auditing |

It develops social accounting as an assessment tool for social audit to ensure accountability and transparency in corporate governance and decision-making structures. |

|

1 |

60 |

0.908 |

2016 |

Social Value |

Studies used a polyhedral model to identify and quantify the social value of stakeholder groups by using qualitative and quantitative methodologies. |

|

2 |

48 |

0.991 |

2010 |

Micro-Economy |

Using a social accounting matrix to address the micro-economic factors and their impacts |

|

3 |

36 |

0.906 |

2011 |

Public Policy |

Studies on the multiplier model of social accounting in order to construct social policy. |

|

4 |

33 |

0.875 |

2007 |

Stakeholder Policy and Practice |

Analyze stakeholder theories in relation to social accounting and develop policies to address stakeholder issues. |

|

5 |

29 |

0.991 |

2011 |

Economic Output |

Studies on the social accounting matrix in the specific case of the Alaska seafood industry to measure economic output |

|

6 |

29 |

0.993 |

2015 |

Energy Policy |

Social accounting that incorporates the objectives of energy policies like carbon pricing, CO2 emissions and the environment. |

|

7 |

28 |

0.988 |

2015 |

Social and Environmental Sustainability |

Analysis of social accounting literature and highlights the various SEA challenges |

|

8 |

28 |

0.987 |

2014 |

Social Economy |

To structure the social economy, conduct research on social and economic interests in order to move forward with social entrepreneurship and economy for the common good. |

|

9 |

25 |

0.95 |

2013 |

Social Return on Investment |

Case study analysis highlights the challenges in social accounting under the methodology framework for calculating the social return on investment. |

|

10 |

21 |

0.945 |

2008 |

Corporate Disclosure |

Studies examine the annual reports to determine to what extent firms' reports truly depict their SEA disclosure policies and practices. |

|

11 |

13 |

0.99 |

2009 |

Corporate Social Responsibilities |

Analysis of social accounting procedures in relation to the corporate social responsibilities of the firms |

Silhouette: quality of a clustering configuration (Rousseeuw, 1987), suggested parameters between 0.7 and 1 (Chen et al., 2010). Source: authors’ own elaboration.

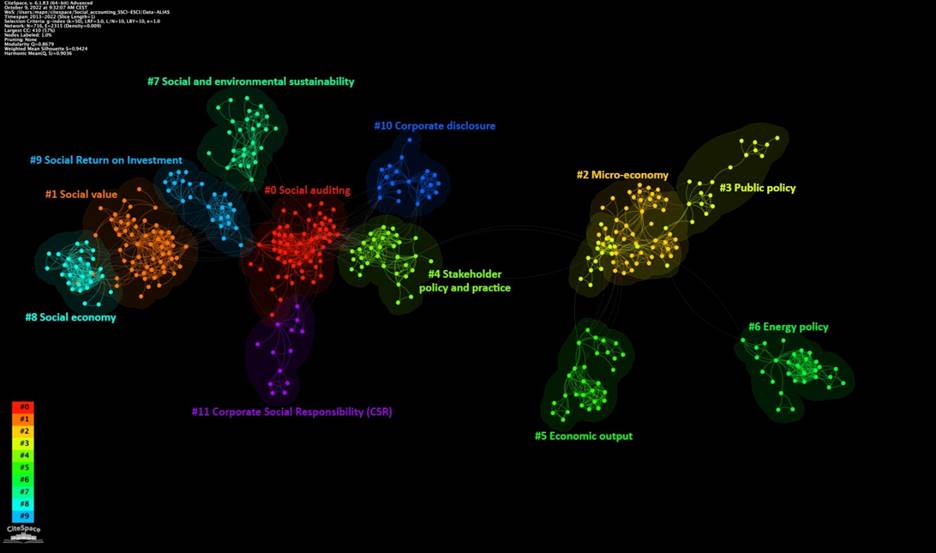

All clusters have a certain silhouette value, which determines the strength of each cluster in the network. To choose the appropriate number of clusters, the silhouette value must fall between the range of 0.7 and 1.0 (Chen et al., 2010). The silhouette value of most clusters that were created has a greater value than 0.9 except for clusters 0 and 4, which have a value of 0.893 and 0.875, respectively. This indicates that all the clusters have strong homogeneity. Similarly, higher Modularity Q value of 0.8679 means each cluster has clear boundaries and the network is well structured (Chen et al., 2009). The network for SA is shown in figure 2.

Fig. 2 Social accounting co-citation network. Source: authors’ own elaboration.

However, the main limitations and drawbacks in the interpretation of clusters and the identification of the core theme of each cluster depend on the analyst’s own domain of knowledge, experiences and expertise. As a result, distinguishing between evidence-based findings and speculations and heuristics may be difficult (Zupic and Cater, 2015). To summarise each cluster's key characteristics and to strengthen the reliability of the co-citation cluster labelling procedure, both the common ties between researchers in each cluster and the citations have been examined.

Cluster #0 focuses on social auditing. Social audits provide an opportunity for individuals to enforce accountability and transparency, giving the ultimate user a chance to examine the development activities or initiatives. In this area of knowledge, researchers reported that social accounts should be maintained independently from businesses (Gray et al., 2014) and promote more social equality (Cooper et al., 2005). However, Thomson et al. (2015) argued that the use of external accounting exhibits significant potential for any organisation when combined with holistic strategies, even when competing with strong multi-national corporations. On the other hand, Brown (2009) considers the democratic theory for the development of dialogic accounting, where diversity is respected and valued while treating ideological and interpretative disparities seriously in the decision-making process.

Cluster #1 is based on the social value created by the organisation; a SA model helps to integrate social and economic values. The polyhedral model makes it possible to monetise the specific social value of the stakeholders by combining qualitative and quantitative approaches (Ayuso et al., 2020; Lazcano et al., 2019; Retolaza et al., 2014, 2015). The qualitative approach is based on the stakeholder theory (Freeman, 1984), an expanded concept, and involves engaging in dialogue among all the stakeholders to visualise the perceived value. The quantitative approach used to monetise the perceived value involves using indicators and proxy variables.

Cluster #2 has to do with micro-economy, specifically with how the SAM framework addresses economic factors and its impacts. Hartono and Resosudarmo (2008) and Akkemik (2011) examine how the efficient utilisation of energy (electricity) consumption produces a wider impact on the economy, while being specific to government subsidy policies, households’ income and business activities. Agostini et al. (2010) examined the subject's relevance so as to understand the cause of poverty and its distribution across native and non-native households to define government relief policy. Rodríguez Morilla et al. (2007) used the SAM to examine the economic and environmental strategies.

Cluster #3 deals with SAM framework related to public policy. In this cluster, Akkemik (2012) examines the contribution of international and domestic tourists to economic growth and the role played by the travel and tour operator industries. De Miguel-Velez and Perez (2010) used the multiplier model of the SA framework for the classification of absorption and diffusion effects of household poverty levels in order to construct the social policy. Hertwich and Peters (2009) present specific country CO2 emissions and develop proposals for climate change policy in international trade. Lenzen et al. (2012) propose similar policies to mitigate global climate change and biodiversity loss.

Cluster #4 refers to the Stakeholder policy and practice in SA. Parker (2005) highlights that the implementation of policy and practice in SA must be regulated in combination with various stakeholder, such as governments, corporations and associations of accounting professionals. Dillard and Roslender (2011) recognised the inequitable power relationship in SA from theories and developed policies and practices for the identification and effective allocation of scarce resources by using management accounting and control system tools. O'Dwyer (2005) examines the case study about the stakeholder voices, consultation and engagement in dialogue for accountability. Burritt and Schaltegger (2010) link policies and practice in SA with two different paths of development in sustainable accounting. The first one is the critical path to identify, from the perspective of sustainability accounting, the root of the issues that result in unsustainable development; on the other hand, the managerial path, which emphasised the tools to provide the solutions to the challenges faced by most managers and stakeholders within the organisation.

Cluster #5 deals with the impact on economic output at national and regional level by using various model of SAM specifically with Alaska seafood industry. Seung and Waters (2009) highlight the effects of forward and backward relationship by using the SAM supply driven approach. Seung (2014) examines the supply-side shocks to measure the multi-regional economic impact by using demand-driven SAM. Seung and Waters (2010) study the relevance subject, but this time they analyse the combined effect of supply and demand side shocks on Alaska fisheries by reducing the allowable catch, increasing the energy price and reducing the seafood production. On this occasion, Seung and Waters (2013) examine the regional economic impact and how it will be affected (or bear the cost) by changes in the total allowable catch or the reduction in demand for seafood to protect the endangered species.

Cluster #6 holds the major area of interest in energy policy. Li et al (2014) present and develop the concept of the economic impacts of carbon pricing given that the price of electricity is controlled. To deal with reductions in CO2 emissions, the most effective policy would be carbon pricing. According to Guo et al. (2014), sharp increases in energy prices had an impact on the evaluation of macroeconomic analysis. Aguiar et al. (2016) used the Global Trade Analysis Project (GTAP) database to measure the value of goods and services flowing across the whole world economy with regional and sectoral distribution related environment, energy and economic development.

Cluster #7 mainly focuses on the social and environmental sustainability (SEA) reporting in SA. Deegan (2017) examines SEA literature and highlights the real issues like corporate accountability, satisfying shareholder values and disclosure. Bebbington and Unerman (2018) analyse and evaluate how accounting research contributes to the achievement of the goals established for the sustainable development goals in the United Nations agenda. The agenda outcomes focus on the development of a framework for social justice, environmental concerns and sustainable accounting practices. Belal and Cooper (2011) concentrate on the eco-justice issue and on understanding the factors that make companies reluctant to disclose such issues in corporate reporting.

Cluster #8 offers a particularly relevant bridge between SA and the field of social economy, which is of special interest to the readers of this journal. Porter and Kramer (2011) argue about the conservative view of capitalism and the distribution of economic and social interests. The creation of a social value path is a great opportunity for private and public sectors to be more attracted towards social entrepreneurship, which leads to a global social economy. Chaves Ávila and Monzón Campos (2018) highlight the relevance of the terminology’s social innovation, solidarity economy, collaborative economy, economy for the common good and social enterprise in relation to the emerging paradigm of social economy. In this cluster, several contributions explicitly frame social accounting within the context of social economy organisations. For instance, Retolaza and San-Jose (2016) present a comprehensive model for social accounting as a tool for sustainability, specifically designed to be implemented by entities in the social economy. Their model proposes a system that allows organisations to identify, measure and communicate the social value they generate, not only in monetary terms but also from a stakeholder engagement perspective—emphasising the participatory and democratic ethos that characterises the social economy. Likewise, Etxezarreta Etxarri et al. (2018) apply this model to a case study of a cooperative focused on child welfare, demonstrating how the measurement of social value aligns with the principles of the economy for the common good, social innovation and solidarity economy. These works underline that a significant strand within the literature not only embraces the social economy as a context but sees it as an ideal environment for the development and application of advanced models of social accounting. This confirms that part of the intellectual structure of the field is clearly anchored in the values, goals and practical needs of social economy organisations, making this study particularly relevant for scholars and practitioners working in that domain

Cluster #9 covers the area of the Social Return On Investment (thereinafter, SROI) method in SA. This cluster offers a framework for the analysis of the concept of value under environmental degradation, social inequality and economic cost and benefit. Arvidson et al. (2013) discuss the difficulties encountered when using the SROI approach to account for policymakers, engage stakeholders and ensure accountability. Nicholls et al. (2012) present the basic terminologies and methodology in SROI that help to understand the concept of social value. Arvidson et al. (2010) deliver the relevant subject outline with ambitions and challenges in SA within the SROI methodology framework. They describe how the impact assessment of SROI evolves with the nature of organisations, stakeholder values and managerial behaviours.

The subject of sustainable corporate disclosure in social and environmental reporting is the theme of cluster #10. Gray's (2010) study of the accounting literature for sustainability and corporate sustainable development claims that efficient utilisation of resources, wastage in production and corporate governing bodies' claims about sustainability are not supported by corporate action policies. Abeysekera and Guthrie (2005) examine the annual reports of listed firms to determine to what extent human capital occupies a significant role in firms' annual reporting and disclosure practice. Islam and Deegan (2010) investigate the SEA disclosure reporting policy and practice of firm’s operation influenced by media coverage under employee working environment and child labour. Cheng and Courtenay (2006) address the topic of disclosure and its implications for the nature of the board of directors, the number of directors on the board and the role of CEO duality.

In cluster #11, the last one, the subject of SA and corporate social responsibility (CSR) is addressed. Cooper and Owen (2007) critically assess the extent of institutional (reporting) reform that goes along with voluntary activities to increase corporate accountability by empowering stakeholders. Ackers and Eccles (2015) examine the relevant subject of corporate social reporting with a corporate-level social responsibility assurance framework to understand the stakeholder’s perspective about adequate and reliable CSR reporting. Banerjee (2008) analysed CSR from a critical perspective under the headings of corporate level decision-making structure, corporate hegemony, corporate self-interest and the power of stakeholder partnerships. Likewise, Clarkson et al. (2013) point out that the transparency of environmental reporting was used to determine the firm's performance and value. Unerman and O’Dwyer (2007) analyse the case study of voluntary self-disclosure of CSR and SEA reporting in relation to the corporate decision-making structure while understanding the level of risk faced during the operations.

3.2. Intellectual turning points in Social Accounting

Each published article is represented graphically by a node or dot. Each node that connects with different clusters can be recognised as an intellectual turning point (Chen et al., 2009; Chen and Song, 2019). The importance of a node or dot in bridging the other two nodes is measured by the term "betweenness centrality," which quantifies the number of times a node behaves as if there is a bridge along the shortest distance between other nodes or dots. However, a bibliometric approach considered the fact that betweenness centrality is correlated with long-term future citations of the paper (Shibata et al., 2007).

According to the social network theory, to identify the high central nodes, value for betweenness centrality must be higher than 0.10. Table 3 depicts 7 publications with highest value of betweenness centrality on social accounting subject. These seven papers were considered to be the intellectual backbone of the study, with high betweenness centrality (>0.10). These works act as bridges between different research areas. The research field that spread the most knowledge and have the most intellectual turning points belongs to cluster #0, cluster #3 and cluster #4 with two publications in each cluster. Cluster #2 has only one turning point and the rest of them have no intellectual turning points.

Table 3. Top 3 Intellectual turning point articles in social accounting

|

Centrality |

Cluster |

Author |

Title |

Source |

|

0.31 |

4 |

Parker (2005) |

Social and environmental accountability research: A view from the commentary box |

ACCOUNT AUDIT ACCOUN |

|

0.19 |

3 |

United Nations (2014) |

United Nations, 2014. System of Environmental-economic Accounting 2012 |

SYST ENV EC ACC 2012 |

|

0.15 |

0 |

Gray et al. (2014) |

New accounts: Towards a reframing of social accounting |

ACCOUNT FORUM |

|

0.14 |

0 |

Brown (2009) |

Democracy, sustainability and dialogic accounting technologies: Taking pluralism seriously |

CRIT PERSPECT ACCOUN |

|

0.14 |

3 |

De Miguel-Velez and Perez-Mayo (2010) |

Poverty Reduction and SAM Multipliers: An Evaluation of Public Policies in a Regional Framework |

EUR PLAN STUD |

|

0.13 |

2 |

Miller and Blair (2009) |

"Input-Output Analysis: Foundations and Extensions |

INPUT OUTPUT ANAL FD |

|

0.11 |

4 |

O’Dwyer (2005) |

The construction of a social account: a case study in an overseas aid agency |

ACCOUNT ORG SOC |

Source: authors’ own elaboration.

The highest value of betweenness centrality publication belongs to Parker (2005). Even though SEA subject has been extensively examined by Mathews (1997) and Gray (2002) in their literature review paper covering almost 25 years of SEA research. These papers provide a critical analysis and examination of current research in SEA, specifically reporting policy and practice, which has limited studies, as stated in Mathew and Gray's papers. This study also debates on augmentation theories (stakeholder theory, economic agency theory, decision-usefulness theories) and a group of heartland theories to understand the role of accounting towards environment, economy and social aspects. Finally, the study concludes that the level of academic involvement in the policy and practice aspects of SEA appears bound for ongoing discussion, notably about the academics' perceptions of the threat of the area or subject being taken over by corporations and institutions.

The second highest value for betweenness centrality in the field of SA came from the book “System of Environmental-Economic Accounting 2012 Experimental Ecosystem Accounting” (United Nations, 2014). It focusses on the relationship between humans and the natural environment and has been transformed into ecosystem accounting. Now the corporate world and business entities must look beyond their financial records. They need to look at the effect they are having on environment for sustainable future. This book presented some recommendations on how governments can improve their environmental reporting systems by strengthening coordination among government agencies to improve the quality of data and linking environment and economy in national accounting frameworks to ensure the economic and social benefit.

Thirdly, Gray et al. (2014) examine the newly developing arena of SA as guided by Wright (2006, 2010). Basically, this study investigates whether most of the SA has been, at least traditionally, promoted by accountants, which may be a contributing factor to its self-discipline constraints and, potentially, its weak entry into discourse and practice. This theme is represented as “External Social Audits” in the SA literature, it refers to situations where the accounts are often created by corporations, or specialised entities, or external organisation, or institutions being accounted for. The second theme of the study demonstrate as “New Accounts,” wherein accounts are typically built around, for instance, organisations that have until now largely escaped the attention of SA or, perhaps, have as their focus new notions of the entity about which the account is produced. The authors conclude the potential of the SA project(s) and make the case for the significance of accounts as a tool for interstitial transformation as a complement to the traditional privileging of accounts targeted towards symbiotic transformations.

Fourthly, Brown (2009) analyses the SA to promote and contribute to the theoretical development of dialogic accounting and its limitations. The study recognised the need for new accounting that supports democracy and allows for more participative forms of social organisations or entities. Literature about SEA on sustainable development argues for more dialogical forms of accounting. This study focuses on debates between deliberative and agonistic approach in contemporary political theory to make the case for agonistic to dialogue approach - one that accepts diversity and takes conflicts of interpretation and ideology seriously.

Fifthly, De Miguel-Velez and Perez (2010) used SAM multiplier model to investigate the various public policies effects on poverty alleviation. The study used microsimulation models to assess how public policies affect poverty and disparity and to track the implementation of National Plans for Social Inclusion. The methodology allows researchers to identify the household groups under absorption and diffusion effects. Three different approaches were examined to measure poverty analysis: first, an amount transfer to households whose value is equivalent to certain aids; second, identifying the minimum social expenditure and ensuring that level of household groups; and the third part is poverty reduction diffusion effects.

Sixthly, Miller and Blair (2009) provide a systematic and consistent way to integrate information on environment and economy. It provides a set of accounts and tables that show the relationship between economy and environment, including the flows of goods, services and other resources. The purpose of the framework is to support integrated policy making and decision making, and to enhance understanding of the interdependence between the economy and the environment.

Finally, O’Dwyer (2005) presents a case study to understand how and why the SA process evolves in the Agency for Personal Service Overseas (APSO), an Irish aid agency. APSO examines an in-depth understanding of the SA process, particularly focused on identifying the key stakeholders, their involvement and empowering stakeholder voices. The study conducted an in-depth interview with the board of directors, executive management staff and various stakeholders and reviewed other reports and documents to draft the initial process. The result was shocking to the agency, as management deliberately excluded the voice of stakeholders during the consultation process. The power of management also controlled the voice of the stakeholder group and designed the SA process according to their interests.

3.3. Burst detection in Social Accounting

The most common and appropriate indicators to define the impact of any field of subject on researchers were the number of publications and citation count. Still, we cannot assess the influence, its density and evolution timeframe. To identify the most active research for specific field over a specified period, it is measured by citation burst. Burst detection is an algorithmic tool used to identify changes in a variable in comparison to others within a population during a specific timeframe. CiteSpace software was used in the study to run the specific burst algorithm as introduced by Kleinberg (2003). The algorithm detected that a particular research paper from the population, which was continuously receiving citations (more attention from the academia) within a specified timeframe, is said to be citation burst. Accordingly, it generates a ranked list of publications with the most significant citation bursts with respect to the time intervals in which they occurred. Consequently, a cluster with a sizable number of nodes along with a significant citation burst characterises it as an emergent and active area of research (Chen et al., 2009).

Table 4 shows the outcomes of burst detection analysis and classifies the publications having highest value of citation bursts within the field of social accounting from 2010 to 2022 timeframe. According to the Kleinberg (2003) algorithm, the study found 16 papers with burst citations. All the other papers in the study did not find enough bursts. As shown in Table 4, the burst periods in 2022 were right censored, so we do not know the exact end time frame of the burst periods for these published papers. Social value (cluster #1) is the subject area with the largest number of burst citation papers. Seven papers belonging to the social value cluster show a strong citation burst. Social auditing (cluster #0), micro-economy (cluster #2) and stakeholder policy and practice (cluster #4) each have two burst papers. The average number of burst papers in each cluster is 1.33. Moreover, clusters #3, #8 and #10 have only one burst paper; consequently, only 7 clusters out of 12 have burst publications.

Table 4. Burst papers in social accounting

|

Cluster |

References |

Strength |

Begin |

End |

2011 - 2022 |

|

10 |

Gray (2010) |

3.05 |

2013 |

2015 |

▂▂▃▃▃▂▂▂▂▂▂▂ |

|

4 |

Parker (2005) |

2.71 |

2013 |

2014 |

▂▂▃▃▂▂▂▂▂▂▂▂ |

|

0 |

Cooper et al. (2005) |

2.62 |

2013 |

2015 |

▂▂▃▃▃▂▂▂▂▂▂▂ |

|

4 |

Dillard & Roslender (2011) |

2.5 |

2013 |

2016 |

▂▂▃▃▃▃▂▂▂▂▂▂ |

|

2 |

Miller and Blair (2009) |

4.88 |

2014 |

2019 |

▂▂▂▃▃▃▃▃▃▂▂▂ |

|

2 |

Hartono & Resosudarmo (2008) |

3.15 |

2016 |

2017 |

▂▂▂▂▂▃▃▂▂▂▂▂ |

|

3 |

Akkemik (2012) |

2.98 |

2017 |

2018 |

▂▂▂▂▂▂▃▃▂▂▂▂ |

|

0 |

Thomson et al. (2015) |

2.57 |

2017 |

2019 |

▂▂▂▂▂▂▃▃▃▂▂▂ |

|

1 |

Retolaza et al. (2015) |

4.57 |

2020 |

2022 |

▂▂▂▂▂▂▂▂▂▃▃▃ |

|

1 |

Ayuso et al. (2020) |

3.95 |

2020 |

2022 |

▂▂▂▂▂▂▂▂▂▃▃▃ |

|

8 |

Porter and Kramer (2011) |

3.8 |

2020 |

2022 |

▂▂▂▂▂▂▂▂▂▃▃▃ |

|

1 |

Retolaza et al. (2014) |

3.8 |

2020 |

2022 |

▂▂▂▂▂▂▂▂▂▃▃▃ |

|

1 |

Lazcano et al. (2019) |

3.65 |

2020 |

2022 |

▂▂▂▂▂▂▂▂▂▃▃▃ |

|

1 |

Retolaza & San-José (2018) |

3.42 |

2020 |

2022 |

▂▂▂▂▂▂▂▂▂▃▃▃ |

|

1 |

Retolaza et al. (2020) |

2.73 |

2020 |

2022 |

▂▂▂▂▂▂▂▂▂▃▃▃ |

|

1 |

Retolaza & San-José (2011) |

2.65 |

2020 |

2022 |

▂▂▂▂▂▂▂▂▂▃▃▃ |

Source: authors’ own elaboration.

These study’s research publications were all written between 2005 and 2022 (the intellectual structure analysed is comprised of cited and not citing papers). The average number of burst publications within the time period 2010–2016 was 1.34 per year. After 2017–2022, the average was 0.5 paper each year. After 2020, there will be an increasing trend of research publications exploring the SA subject, which emphasises that the academic and scientific communities have increased interest in the relevant field. In the years 2011, 2015 and 2020, the number of burst papers was more than one, i.e., three publications in 2011 and two in each of the respective years. This means that 2011 was the most prolific year in terms of burst papers. The time elapsed between the publication of burst citation papers and their peak of interest is about 2.06 years. Two research publications were found to have burst their papers in the very same year in which they were published (Ayuso et al., 2020; Retolaza et al., 2020). Moreover, only one burst paper just one year after its publication (Lazcano et al., 2019). Miller and Blair's (2009) research paper have the longest period burst (5 years). Interestingly, 8 out of 16 burst publications have a start burst period in 2020, but its end burst period must still be defined in the future given that the end period of being burst is 2022.

According to Hou et al. (2018), burst analysis can be used to comprehend the most current trends and advancements in a subject of study. Accordingly, there have been seven patterns and trends in the SA discipline. Table 5 shows all seven trends classifying burst papers by cluster, identifying the cluster name, the number of burst papers in the cluster, trend started year (Min(year)) and when it finished (Max(year)), the mean year, the mean strength value, the trend starting year (Min(begin)) and the trend finishing year (Max(end)).

Table 5. Burst papers per cluster in social accounting research

|

Cluster |

Cluster label |

No. Papers |

Min (year) |

Max (year) |

Mean (year) |

Mean (strength*) |

Min (begin) |

Max (end) |

2011-2022** |

|

4 |

Stakeholder Policy & Practice |

2 |

2005 |

2011 |

2008 |

2,61 |

2013 |

2016 |

▂▂▃▃▃▃▂▂▂▂▂▂ |

|

0 |

Social Auditing |

2 |

2005 |

2015 |

2010 |

2,60 |

2013 |

2019 |

▂▂▃▃▃▃▃▃▃▂▂▂ |

|

10 |

Corporate Disclosure |

1 |

2010 |

2010 |

2010 |

3,05 |

2013 |

2015 |

▂▂▃▃▃▂▂▂▂▂▂▂ |

|

2 |

Micro-Economy |

2 |

2008 |

2009 |

2009 |

4,02 |

2014 |

2019 |

▂▂▂▃▃▃▃▃▃▂▂▂ |

|

3 |

Public Policy |

1 |

2012 |

2012 |

2012 |

2,98 |

2017 |

2018 |

▂▂▂▂▂▂▃▃▂▂▂▂ |

|

8 |

Social Economy |

1 |

2011 |

2011 |

2011 |

3,80 |

2020 |

2022 |

▂▂▂▂▂▂▂▂▂▃▃▃ |

|

1 |

Social Value |

7 |

2011 |

2020 |

2017 |

3,54 |

2020 |

2022 |

▂▂▂▂▂▂▂▂▂▃▃▃ |

|

* Mean strength of the burst of a documents of the cluster based on the Kleinberg’s algorithm (2003). |

|||||||||

|

** Red line segment represents the mean time period in which a cluster was found to have a burst, indicating the minimum beginning year and the maximum ending year of the duration of the burst in a cluster. |

|||||||||

Source: authors’ own elaboration.

The result in Table 5 indicates that the initial trend started with Cluster #4, "Stakeholder Policy and Practice," which includes two research papers. The publication of the cluster of burst papers started in 2005 and finished in 2011. However, these publications became burst from 2013 to 2016. In this period, the main research interest evolves from the work of Dillard and Roslender (2011) in the field of management accounting and control systems. Parker's (2005) paper also attempts to contribute to the overall evolution of cluster #4, but it only takes one year of burst. As stakeholder policy and practice become a broader area of interest, it broadens the scope of the authors' other publications. This is one of the primary reasons why cluster #4's burst period is finished in four years.

The second trend also includes two papers from "Social Auditing" in cluster #0. The publication of burst papers began in 2005, like cluster #4, but it took a longer period to complete (2015), and the burst periods for these publications ranged from 2013 to 2019. Cooper's (2005) research work on the line to promote social equality became the publication that marked the beginning of the evolution of cluster bursting. The second burst publication kicked off to continue the cluster burst period with Thomson et al. (2015) related to the use of external accounting with holistic strategies. The main reason behind the decline in the social auditing cluster boom period is its diversification of research towards social value (Cluster #1) and environmental issues (Cluster #7).

The third drift encompasses one single publication (Gray, 2010) that belongs to cluster #10 (Corporate Disclosure) and its burst period started and ended in 2019. The trend deals with lines of research in SA reporting contexts, mainly social and environmental. Gray (2010), with his passion for challenging environmental degradation and social injustice, laid the foundations for the field of SEA research and practice. Moreover, the main reason for the decline in the cluster-burst period was the death of Prof. Rob Gray.

The fourth area of trend includes two papers written in 2008 and 2009 that deal with "micro economy" (Cluster #2). This cluster has the second largest trend in burst papers from 2014 to 2019. Cluster #2 includes Miller and Blair (2009), which is a statistical framework between environmental accounting and economy. This is the only burst publication that has the longest period of burst out of all the burst publications. While Hartono and Resosudarmo (2008) examine the efficient utilisation of energy (electricity) consumption, it produces a wider impact on the economy and has a burst period between 2016 and 2017.

The fifth trend, "Public Policy," belongs to cluster #3. It has only one paper (Akkemik, 2012) and, after five years, it became a burst paper for the period of 2017 and 2018.

The sixth drift of publication was written in 2011, having a single paper (Porter and Kramer, 2011) that dealt with "Social Economy" (Cluster #8), became a burst publication in 2020 and is still a burst publication in 2022.

Lastly, the seventh trend deals with the largest number of publications, where seven papers written between 2011 and 2020 became bursts in 2016 and were still bursts when these publications were written in the year 2020. This trend is related to "social value" (cluster #1) and will continue in the future as a burst papers cluster. The first burst paper was written by Retolaza and San-José (2011), on social economy and stakeholder theory and a series of burst papers were published by both authors, i.e., quantification of social value (Retolaza et al., 2014), monetasing the social value (2015) and SA and organisational behaviour (2020). Thus, the majority of the papers published by Retolaza and San-Jose's scientific group were in cluster #1 (Social Value), and all of these publications were in the category of burst publications and the cluster burst is still ongoing.

All in all, the first four trends, that overlap each other in time, reveal that academia and researchers initially developed a strong interest in achieving eminently theoretical knowledge in the shape of Stakeholder theory policy and practice (cluster #4), social auditing (cluster #0), Corporate Disclosure (cluster #10) and micro economy (cluster #2) in the SA discipline. However, cluster #2 has been the longest burst over the 6 years (2014-2019) and it also has the highest strength mean. The sixth (cluster #8) and seventh (cluster #1) trends are still burst in 2022 (when this paper was written). The trends that show higher level of interest over the last ten years is social value (Cluster #1), which is the largest one in terms of number of burst papers, and each and every of these seven papers are still burst in 2022.

Out of the data obtained in the study, 10 thematic areas of research are identified, which should give rise to ten specific agendas corresponding to the positioning of each researcher in any of the thematic clusters. Nonetheless, the overall analysis provides us with some hints concerning possible lines of research; in particular, these that can take advantage of the potential for interconnection of several clusters. Considering that the hottest cluster is the one related to social value (cluster #1), it is conceivable that the most promising lines of research may be related to this topic. The standardisation of procedures for the identification and accounting of social value, particularly in monetary units, should be the main line of research; in continuation of the most updated papers. In this area of research, the analysis of cases, the comparison of models and the discussion of a universal system for understanding and transferring information are topics that are still in their early stages of development and have great potential for further development.

Complementary, but no less important, are the lines of research connecting nearby clusters. In this sense, it is worth mentioning the closeness between the social value cluster (#1) and the SROI cluster (#9). If we focus on the analysis of the latest papers published in relation to SROI, we notice that there is a shift from the analysis of return on investment/projects to the analysis of organisational impact (Arenas et al., 2022). Despite the fact that these papers are heirs to SROI—and thus employing the terminology and references of this cluster—they are dealing with SA issues, which are best categorised as cluster #1. This highlights the need for a line of research that brings together the main contributions of both clusters, providing a solution that integrates the value generated by organisations or investments under the same framework, but in a differentiated way.

It is also possible to visualise a line of research that connects social value with previous research on the subject, which is mainly found in clusters #0 (Social Auditing) and #7 (Social and Environmental Sustainability). Even though it is also close, cluster #11 (CSR) seems to be clearly in decline and, although it might be interesting to establish some historical connection in theoretical frameworks, it does not seem to be a promising line of research.

The one that certainly looks promising as a line of research is the interconnection between social value (#1) and social economy (#1); as the study shows, these are the two most topical clusters and are already linked by joint works, which is quite different from the rest of clusters.

Complementary to these specific and promising lines of research, perhaps the integration of the research carried out in clusters #1, #8, #9 #7, #0 and #11 will allow the development of a systematic theoretical framework that will allow society to visualise in a understandable way the social strategies that companies carry out to strengthen their link with the cluster; and its differentiation from other research areas which, although related, are quite distant, such as clusters #2 (Micro-economy), #3 (Public policy and Practice), #5 (Economic output) and #6 (Energy policy).

· How can artificial intelligence be used to automate the identification, classification and monetisation of social value in organisational contexts?

· What methodologies can improve the comparability of different social accounting models applied to social economy organisations?

· What are the effects of adopting real-time or dynamic social accounting systems, integrating updated stakeholder feedback?

· How can big data techniques support predictive analysis in the field of social value creation and its distribution among stakeholders?

· What are the limitations and opportunities in using natural language processing to extract social impact indicators from narrative reports?

Firstly, some studies have delineated the core and active research fields within the discipline of SA: social auditing, social value, micro-economy, public policy, stakeholder policy and practice, economic output, energy policy, social and environmental sustainability, social economy, SROI, corporate disclosure and CSR.

Secondly, the research publications that develop the intellectual backbone of SA field have been identified. The knowledge of the research area is built on the turning points. When they are identified, academia can learn more about the area and more quickly, including how to begin their own research. For instance, researchers who want to know about Social Auditing (Cluster #0) so as to understand the objective, principles and future direction, should start their literature review by reading the articles of Gray et al. (2014) and Brown (2009). These papers serve as a foundational basis for advancing knowledge of future research in specific discipline. As a result, this procedure remarkably saves the time and effort of researchers, particularly during the initial stages of developing the conceptual framework of the research, because the field’s engines for knowledge were taken as reference.

Thirdly, this study identified some burst papers, those papers that received a lot of attention from the scientific community in each period. Finding burst papers provides an overview of the evolving state of the literature on SA with respect to each burst papers. At this stage, it is a crucial finding because it gives academics the direction in which they need to move for future research.

The theoretical implications of the paper include the identification of the paradigms and research methodologies underlying SA, which complement the literature mapping. Thus, it was determined that SA is a multifaceted field that permits a variety of research methodologies and paradigms to be used, allowing for a greater theoretical and practical depth of the analysed themes. This means that the study of SA can be approached critically when attempting to address the challenges of social value posed by factors such as quantification of social value (Retolaza et al., 2014), monetasing the social value (Retolaza et al., 2015) and SA and organisational behaviour (Retolaza et al., 2020). Thus, most of the papers published by Retolaza and San-Jose's scientific group were in cluster #1 (Social Value), and all these publications were in the category of burst publications and the cluster burst is still ongoing.

A huge volume of data can benefit from the bibliometric analysist' ability to organise it in a meaningful way so that accurate quantitative and approximatively qualitative evaluations can be drawn. Yet, it also has some restrictions that have persisted for a long time. To interpret the findings of the analysis, a high level of involvement and, consequently, subjective participation of the analysts is required. Therefore, bibliometric techniques must be used in conjunction with intellectual refinement, which calls for activities like a thorough review of the literature on the topic, its synthesis and/or a discussion among academics (Zupic and Cater, 2015). To obtain a trustworthy set of indicators that could be used to come to some sort of reasonable conclusions, the researcher must make some technical decisions regarding the parameters of the chosen database and the analytical software (e.g., limitations of language, journals, time period, normalisation of cluster labelling, verification of final data to debug errors, etc.).

In conclusion, this study not only provides a comprehensive map of the intellectual structure of social accounting, but also highlights the dynamic evolution and diversification of the field over the past decade. The co-citation analysis reveals how core concepts such as social value, stakeholder engagement and social return on investment have become central pillars, shaping both theoretical and practical approaches. As social accounting gains traction across diverse organisational contexts, future research must continue to explore innovative methodologies and interdisciplinary frameworks to address emerging challenges. Ultimately, this paper aims to serve as both a reference point and a catalyst for advancing scholarly dialogue and practical applications within the growing domain of social accounting.

The authors declare no conflict of interest.

Ali Faiz: Conceptualisation, Methodology, Software, Validation, Formal analysis, Investigation, Resources, Data Curation, Writing - Original Draft, Writing - Review & Editing, Visualization, Funding acquisition. Miquel-Angel Plaza-Navas: Conceptualisation, Methodology, Software, Validation, Formal analysis, Investigation, Resources, Data Curation, Writing - Original Draft, Writing - Review & Editing, Visualization. Miguel Prado-Román: Investigation, Resources, Writing - Review & Editing, Visualization. Jose Torres-Pruñonosa: Conceptualisation, Methodology, Software, Validation, Formal analysis, Investigation, Resources, Data Curation, Writing - Original Draft, Writing - Review & Editing, Visualization, Supervision, Project administration, Funding acquisition.

Funding

This work was supported by Universidad Internacional de la Rioja (PP-2021-06 and PP-2023-10) and Fundació UAB (Universitat Autònoma de Barcelona).

Abeysekera, I. and Guthrie, J. (2005). An empirical investigation of annual reporting trends of intellectual capital in Sri Lanka, Critical Perspectives on Accounting, Vol. 16 No. 3, pp. 151–163, doi: 10.1016/S1045-2354(03)00059-5.

Ackers, B. and Eccles, N.S. (2015). Mandatory corporate social responsibility assurance practices: The case of King III in South Africa, Accounting, Auditing & Accountability Journal, Vol. 28 No. 4, pp. 515–550, doi: 10.1108/AAAJ-12-2013-1554.

Agostini, C.A., Brown, P.H. and Roman, A.C. (2010). Poverty and Inequality Among Ethnic Groups in Chile, World Development, Vol. 38 No. 7, pp. 1036–1046, doi: 10.1016/j.worlddev.2009.12.008.

Aguiar, A., Narayanan, B. and McDougall, R. (2016). An Overview of the GTAP 9 Data Base, Journal of Global Economic Analysis, Vol. 1 No. 1, pp. 181–208, doi: 10.21642/JGEA.010103AF.

Akkemik, K.A. (2011). Potential impacts of electricity price changes on price formation in the economy: a social accounting matrix price modeling analysis for Turkey, Energy Policy, Vol. 39 No. 2, pp. 854–864, doi: 10.1016/j.enpol.2010.11.005.

Akkemik, K.A. (2012). Assessing the importance of international tourism for the Turkish economy: A social accounting matrix analysis, Tourism Management, Vol. 33 No. 4, pp. 790–801, doi: 10.1016/j.tourman.2011.09.002.

Arenas, M. C., Sánchez-Infante Hernández, M. V. and Sánchez-González, G. (2022). The social return on investment model: A systematic literature review, Meditari Accountancy Research, Vol. 30 No. 7, pp. 1663–1685, doi: 10.1108/MEDAR-05-2021-1307.

Arvidson, M., Lyon, F., McKay, S. and Moro, D. (2010). The Ambitions and Challenges of SROI, TSRC, Third Sector Research Centre.

Arvidson, M., Lyon, F., McKay, S. and Moro, D. (2013). Valuing the social? The nature and controversies of measuring social return on investment (SROI), Voluntary Sector Review, Vol. 4 No. 1, pp. 3–18, doi: 10.1332/204080513X661554.

Ayuso, S., Sánchez, P., Retolaza, J.L. and Figueras-Maz, M. (2020). Social value analysis: the case of Pompeu Fabra University, Sustainability Accounting, Management and Policy Journal, Vol. 11 No. 1, pp. 233–252, doi: 10.1108/SAMPJ-11-2018-0307.

Baker, M., Gray, R. and Schaltegger, S. (2023). Debating accounting and sustainability: from incompatibility to rapprochement in the pursuit of corporate sustainability, Accounting, Auditing & Accountability Journal, Vol. 36 No. 2, pp. 591-619, doi: 10.1108/AAAJ-04-2022-5773.

Banerjee, S.B. (2008). Corporate Social Responsibility: The Good, the Bad and the Ugly, Critical Sociology, Vol. 34 No. 1, pp. 51–79, doi: 10.1177/0896920507084623.

Bebbington, J. and Unerman, J. (2018). Achieving the United Nations Sustainable Development Goals: An enabling role for accounting research, Accounting, Auditing & Accountability Journal, Vol. 31 No. 1, pp. 2–24, doi: 10.1108/AAAJ-05-2017-2929.

Belal, A.R. and Cooper, S. (2011). The absence of corporate social responsibility reporting in Bangladesh, Critical Perspectives on Accounting, Vol. 22 No. 7, pp. 654–667, doi: 10.1016/j.cpa.2010.06.020.

Brown, J. (2009). Democracy, sustainability and dialogic accounting technologies: Taking pluralism seriously, Critical Perspectives on Accounting, Vol. 20 No. 3, pp. 313–342, doi: 10.1016/j.cpa.2008.08.002.

Burritt, R.L. and Schaltegger, S. (2010). Sustainability accounting and reporting: fad or trend?, Accounting, Auditing & Accountability Journal, Vol. 23 No. 7, pp. 829–846, doi: 10.1108/09513571011080144.

Carnegie, G.D., Gomes, D., Parker, L.D., McBride, K. and Tsahuridu, E. (2024). How accounting can shape a better world: framework, analysis and research agenda, Meditari Accountancy Research, Vol. 32 No. 5, pp. 1529-1555, doi:10.1108/MEDAR-06-2024-2509

Chaudhuri, C., Pratap, D. and Pohit, S. (2024). Estimation of SAM for India: An Application for India’s Energy Transition Targets. Margin: The Journal of Applied Economic Research, Vol. 18 No. 1-2, pp. 74-133, doi:10.1177/00252921241284278

Chaves Ávila, R. and Monzón Campos, J.L. (2018). La economía social ante los paradigmas económicos emergentes: innovación social, economía colaborativa, economía circular, responsabilidad social empresarial, economía del bien común, empresa social y economía solidaria, CIRIEC-España, revista de economía pública, social y cooperativa, No. 93, pp. 5–50, doi: 10.7203/CIRIEC-E.93.12901.

Chen, C. (2017). Science Mapping: A Systematic Review of the Literature, Journal of Data and Information Science, Vol. 2 No. 2, pp. 1–40, doi: 10.1515/jdis-2017-0006.

Chen, C., Chen, Y., Horowitz, M., Hou, H., Liu, Z. and Pellegrino, D. (2009). Towards an Explanatory and Computational Theory of Scientific Discovery, Journal of Informetrics, Vol. 3 No. 3, pp. 191–209, doi: 10.1016/j.joi.2009.03.004.

Chen, C., Ibekwe-SanJuan, F. and Hou, J. (2010). The Structure and Dynamics of Cocitation Clusters: A Multiple-Perspective Cocitation Analysis, Journal of the American Society for Information Science and Technology, Vol. 61 No. 7, pp. 1386–1409, doi: 10.1002/asi.21309.

Chen, C. and Song, M. (2019). Visualizing a Field of Research: A Methodology of Systematic Scientometric Reviews, PLoS One, Vol. 14 No. 10, p. e0223994, doi: 10.1371/journal.pone.0223994.

Cheng, E.C.M. and Courtenay, S.M. (2006). Board composition, regulatory regime and voluntary disclosure, The International Journal of Accounting, Vol. 41 No. 3, pp. 262–289, doi: 10.1016/j.intacc.2006.07.001.

Clarkson, P.M., Fang, X., Li, Y. and Richardson, G. (2013). The relevance of environmental disclosures: Are such disclosures incrementally informative?, Journal of Accounting and Public Policy, Vol. 32 No. 5, pp. 410–431, doi: 10.1016/j.jaccpubpol.2013.06.008.

Cooper, C., Taylor, P., Smith, N. and Catchpowle, L. (2005). A discussion of the political potential of Social Accounting, Critical Perspectives on Accounting, Vol. 16 No. 7, pp. 951–974, doi: 10.1016/j.cpa.2003.09.003.

Cooper, S.M. and Owen, D.L. (2007). Corporate social reporting and stakeholder accountability: The missing link, Accounting, Organizations and Society, Vol. 32 No. 7–8, pp. 649–667, doi: 10.1016/j.aos.2007.02.001.

De Miguel-Velez, F.J. and Perez-Mayo, J. (2010). Poverty Reduction and SAM Multipliers: An Evaluation of Public Policies in a Regional Framework, European Planning Studies, Vol. 18 No. 3, pp. 449–466, doi: 10.1080/09654310903497751.

Deegan, C. (2017). Twenty five years of social and environmental accounting research within Critical Perspectives of Accounting : Hits, misses and ways forward, Critical Perspectives on Accounting, Vol. 43, pp. 65–87, doi: 10.1016/j.cpa.2016.06.005.

Díez-Martín, F., Blanco-González, A. and Prado-Román, C. (2020). The Intellectual Structure of Organizational Legitimacy Research: A Co-Citation Analysis in Business Journals, Review of Managerial Science, Vol. 15, pp. 1007–1043, doi: 10.1007/s11846-020-00380-6.

Dillard, J. and Roslender, R. (2011). Taking pluralism seriously: Embedded moralities in management accounting and control systems, Critical Perspectives on Accounting, Vol. 22 No. 2, pp. 135–147, doi: 10.1016/j.cpa.2010.06.014.

Donthu, N., Kumar, S., Mukherjee, D., Pandey, N. and Lim, W. M. (2021). How to conduct a bibliometric analysis: An overview and guidelines, Journal of Business Research, Vol. 133, pp. 285–296, doi: 10.1016/j.jbusres.2021.04.070

Echanove-Franco, A., San-Jose, L. and Retolaza, J. L. (2023). Design of a protocol model for the integration of social value in strategic management through social accounting, Social Responsibility Journal, Vol. 20 No. 1, pp. 108-127, doi: 10.1108/srj-12-2022-0551.

Egghe, L. (2006). Theory and Practise of the g-index, Scientometrics, Vol. 69 No. 1, pp. 131–152, doi: 10.1007/s11192-006-0144-7.

Escamilla-Solano, S., Flores-Ureba, S., Sánchez-De Lara, M. Á., & Gómez-Ortega, A. (2025). Intellectual structure of social accounting research: a co-citation analysis in business economics, Total Quality Management & Business Excellence, Vol. 36, No. 5–6, pp. 572–589, doi: 10.1080/14783363.2025.2471851

Etxezarreta Etxarri, E., Pérez de Mendiguren Castresana, J.C., Diaz Molina, L. and Errasti Amozarrain, A. (2018). Valor social de las cooperativas sociales: aplicación del modelo poliédrico en la cooperativa para la acogida de menores Zabalduz S.Coop, CIRIEC-España, Revista de Economía Pública, Social y Cooperativa, No. 93, pp. 155–180, doi: 10.7203/CIRIEC-E.93.9953.

Freeman, R.E. (1984). Strategic Management: A Stakeholder Approach, Pitman, Boston.

Freeman, E., Retolaza, J. L., & San José, L. (2020). Stakeholder Accounting: hacia un modelo ampliado de contabilidad. CIRIEC-España, Revista de economía Pública, Social y Cooperativa, No. 100, pp. 89–114, doi: 10.7203/CIRIEC-E.100.18962

Gray, R. (1992). Accounting and environmentalism: An exploration of the challenge of gently accounting for accountability, transparency and sustainability, Accounting, Organizations and Society, Vol. 17 No. 5, pp. 399–425, doi: 10.1016/0361-3682(92)90038-T.

Gray, R. (2002). The social accounting project and Accounting Organizations and Society Privileging engagement, imaginings, new accountings and pragmatism over critique?, Accounting, Organizations and Society, Vol. 27 No. 7, pp. 687–708, doi: 10.1016/S0361-3682(00)00003-9.

Gray, R. (2010). Is accounting for sustainability actually accounting for sustainability…and how would we know? An exploration of narratives of organisations and the planet, Accounting, Organizations and Society, Vol. 35 No. 1, pp. 47–62, doi: 10.1016/j.aos.2009.04.006.

Gray, R., Brennan, A. and Malpas, J. (2014). New accounts: Towards a reframing of social accounting, Accounting Forum, Vol. 38 No. 4, pp. 258–273, doi: 10.1016/j.accfor.2013.10.005.

Guo, Z., Zhang, X., Zheng, Y. and Rao, R. (2014). Exploring the impacts of a carbon tax on the Chinese economy using a CGE model with a detailed disaggregation of energy sectors, Energy Economics, Vol. 45, pp. 455–462, doi: 10.1016/j.eneco.2014.08.016.

Hartono, D. and Resosudarmo, B.P. (2008). The economy-wide impact of controlling energy consumption in Indonesia: An analysis using a Social Accounting Matrix framework, Energy Policy, Vol. 36 No. 4, pp. 1404–1419, doi: 10.1016/j.enpol.2007.12.011.

Hertwich, E.G. and Peters, G.P. (2009). Carbon Footprint of Nations: A Global, Trade-Linked Analysis. Environmental Science & Technology, Vol. 43 No. 16, pp. 6414–6420, doi: 10.1021/es803496a.

Hietschold, N., Voegtlin, C., Scherer, A.G. and Gehman, J. (2023). Pathways to social value and social change: An integrative review of the social entrepreneurship literature, International Journal of Management Reviews, Vol. 25 No. 3, pp. 564–586, doi: 10.1111/ijmr.12321

Hota, P.K., Subramanian, B. and Narayanamurthy, G. (2020). Mapping the Intellectual Structure of Social Entrepreneurship Research: A Citation/Co-citation Analysis. Journal of Business Ethics, Vol. 166, pp. 89–114, doi: 10.1007/s10551-019-04129-4

Hou, J., Yang, X. and Chen, C. (2018). Emerging trends and new developments in information science: a document co-citation analysis (2009–2016), Scientometrics, Vol. 115 No. 2, pp. 869–892, doi: 10.1007/s11192-018-2695-9.